BALANCE SHEET

Balance sheet is a statement which shows the financial position i.e. the balances of assets, liabilities and capital, of a business entity at a given date. It is prepared from the real accounts and personal accounts of trial balance. A debit balance in a real account or personal account represents an asset of the concern/firm. Likewise a credit balance in a personal account represents a liability. There can be some newly opened accounts as well on account of adjustment entries. The assets and liabilities are arranged in a proper way and the resultant statement is the balance sheet. On the right hand side, assets are arranged while on the left hand side, liabilities are recorded. The totals of the two sides of the balance sheet must agree because of the equation, viz.

Assets = Liabilities + Capital.

If there is a difference, it means that there is some mistake. The difference, if it does occur, should be placed on the deficit side as Suspense Account to make the two sides agree apparently.

Features of Balance Sheet

– The primary objective of the preparation of balance sheet is to ascertain the financial position of a concern.

– It shows (a) the nature and value of assets, (b) the nature and value of liabilities and (c) the position of capital.

– Balance sheet is always prepared on a certain date, never for a particular period.

– Balance sheet, unlike a trading and profit and loss account, is not an account. It is a statement containing information regarding assets, liabilities and capital.

Marshalling of Balance Sheet

The arrangement of assets and liabilities in accordance with a particular order is known as marshalling of balance sheet. The items in the balance sheet are generally marshalled in two ways-

(i) Liquidity order or according to time: In liquidity order, the assets are stated in the order in which they can be easily converted into cash and the liabilities in the order in which they have to be paid off.

(ii) Permanence order or according to purpose: In permanence order, assets which are to be used permanently in the business and are not meant for sale are shown first and the assets that are liquid are shown last in order. Similarly, liabilities may also be shown according to the permanence arrangement. Specimen of Balance Sheet in permanence order is given below. The order will be reversed in liquidity order.

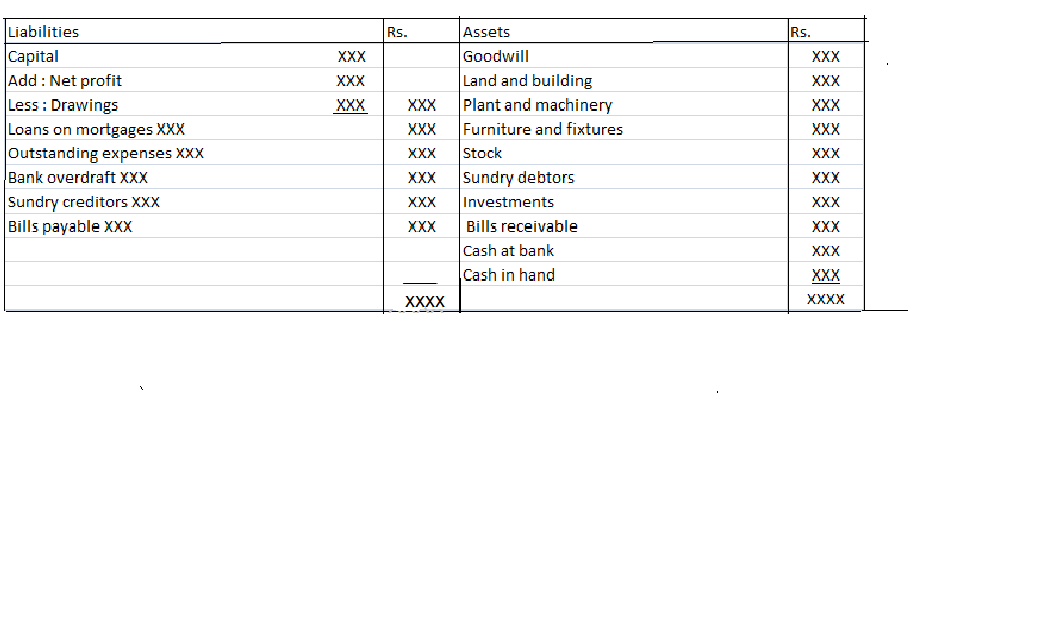

SPECIMEN OF BALANCE SHEET

Balance Sheet as at…