Calculation of Sacrificing Ratio :

In partnership business when a partner is admitted into a firm, the old partners have to surrender a portion of their shares of profits in favour of the new partner. Sacrificing ratio is the difference between old profit sharing ratio and the new profit sharing ratio of the old partners. In this case, sacrifice made by the existing partners may either be in the ratio in which they were sharing profits prior to the admission or in some other ratio :

(i) Besides the old ratio of old partners, if the new ratio of the incoming partners has been given without mentioning the details of the sacrifice made by the old partners, then the presumption is that the old partners have made sacrifice in the old ratio.

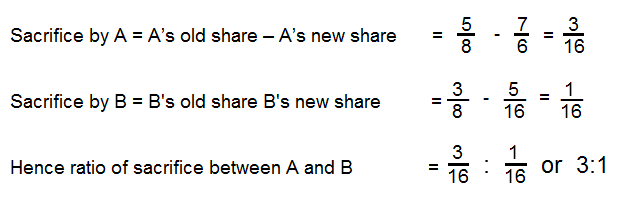

(ii) Sometimes, the new ratio of all the partners and old ratio of old partners are given. In that case sacrificing ratio must be calculated by deducting the new share from the old share of the old partners.

For example, if A and B share profits in the ratio of 5:3 respectively and on admission of C the new ratio among A, B and C is agreed upon as 7:5:4 respectively, the ratio of sacrifice will be calculated as follows: