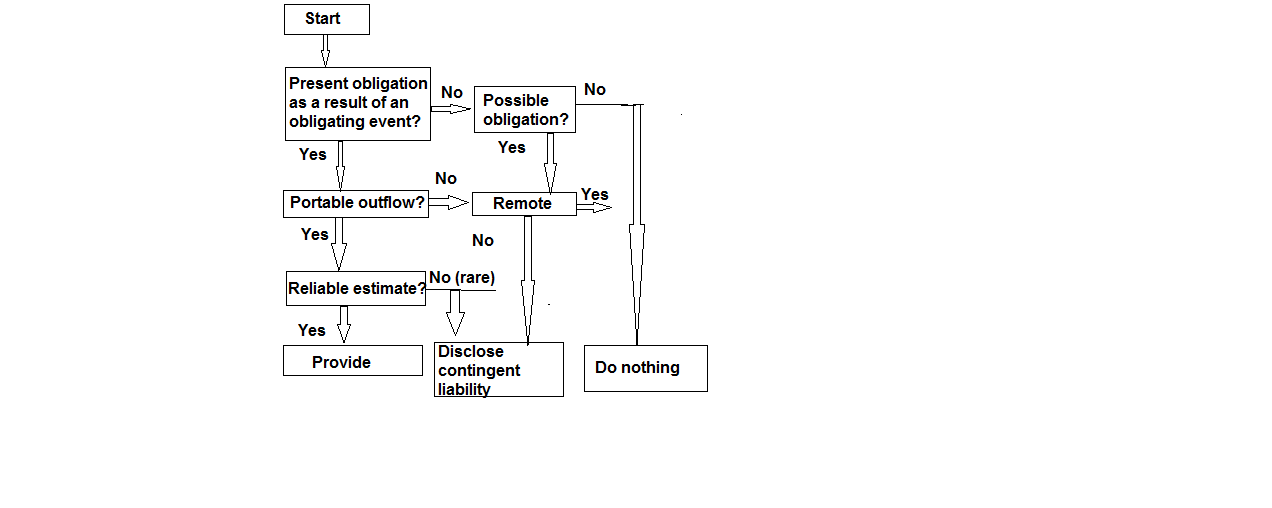

Illustration B

Decision Tree

The purpose of the decision tree is to summarise the main recognition requirements of the Accounting Standard for provisions and contingent liabilities. The decision tree does not form part of the Accounting Standard and should be read in the context of the full text of the Accounting Standard.

Note: in rare cases, it is not clear whether there is a present obligation. In these cases, a past event is deemed to give rise to a present obligation if, taking account of all available evidence, it is more likely than not that a present obligation exists at the balance sheet date (paragraph 15 of the Standard)