Process of accounting :

The process of accounting as per the above definition is given below:

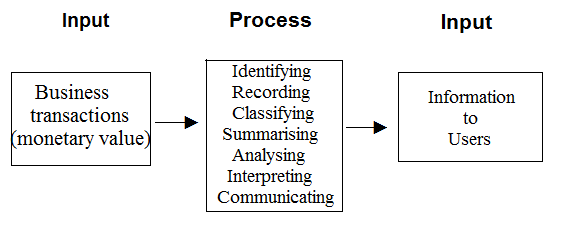

In order to accomplish its main objective of communicating information to the users, accounting embraces the following functions.

i. Identifying: Identifying the business transactions from the source documents.

ii. Recording: The next function of accounting is to keep a systematic record of all business transactions, which are identified in an orderly manner, soon after their occurrence in the journal or subsidiary books.

iii. Classifying: This is concerned with the classification of the recorded business transactions so as to group the transactions of similar type at one place. i.e., in ledger accounts. In order to verify the arithmetical accuracy of the accounts, trial balance is prepared.

iv. Summarising : The classified information available from the trial balance are used to prepare profit and loss account and balance sheet in a manner useful to the users of accounting information.

v. Analysing: It establishes the relationship between the items of the profit and loss account and the balance sheet. The purpose of analysing is to identify the financial strength and weakness of the business. It provides the basis for interpretation.

vi. Interpreting: It is concerned with explaining the meaning and significance of the relationship so established by the analysis. Interpretation should be useful to the users, so as to enable them to take correct decisions.

vii. Communicating: The results obtained from the summarised, analysed and interpreted information are communicated to the interested parties.