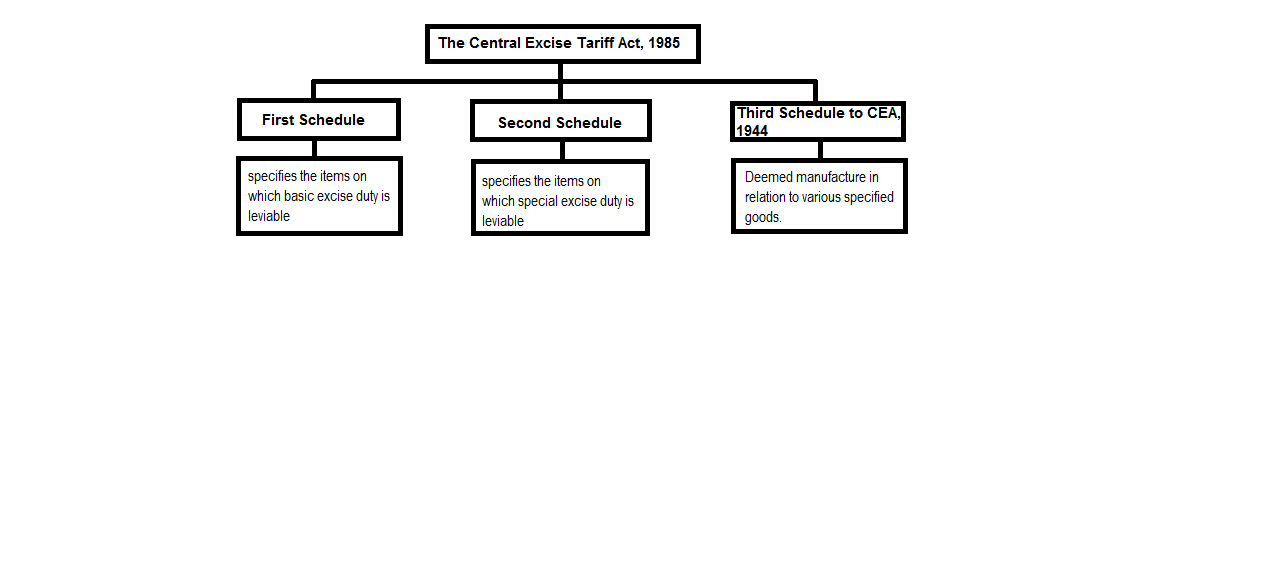

Schedules to tariff :

(a) First Schedule: It consists of 96 chapters and twenty sections. This Schedule provides the rates of basic excise duty (CENVAT) leviable on various products.

(i) Sections: A group of Chapters representing a broad class of goods.

For example, Section I relates to Live animals and Animal products while Section V relates to Mineral products.

(ii) Chapters: Each section is divided into various chapters and sub-chapters.

- Each chapter contains goods of a particular class.

- The chapters are arranged classifying all goods of a kind beginning with the raw material and ending with the finished products, within the same Chapter.

- It is also designed to group all goods relating to the same industry and all goods obtained from the same raw material under one Chapter, in progressive manner.

(iii) Chapter notes: They are mentioned at the beginning of each chapter. These notes have been given statutory backing and have been incorporated at the top of each Chapter.

(iv) Heading: Each chapter and sub-chapter is further divided into various heading depending upon the different types of goods belonging to the same class of products.

(v) Sub-heading: Each heading is further divided into various sub-heading.

(vi) Rules of Interpretation and General explanatory notes

Along the lines of HSN, the Excise tariff has a set of Rules of Interpretation for the interpretation of First schedule and General Explanatory notes.

(i) Rules of interpretation:- Six

(ii) General explanatory notes: Two

(b) Second Schedule: Second Schedule specifies the items on which special excise duty is leviable.

However, with effect from 01.03.2006, all goods have been exempted from special excise duty.

(c) Third Schedule: This schedule specifies goods in relation to which packing, repacking, labeling, re-labelling, MRP declaration/alteration or treatment of goods to render them marketable shall amount to manufacture under section 2(f)(iii) of the Central Excise Act, 1944.