Calculation of Missing Figures :

The information which is needed for preparing the final accounts is not directly available from the incomplete records. Hence, we need to find out such missing figures by preparing relevant accounts. Let us learn how such missing figures can be extracted from incomplete records by preparing the relevant accounts. The important ones are discussed below:

1. Calculation of total purchases or creditors in the beginning or at the end of the year.

2. Calculation of total sales or debtors in the beginning or at the end of the year.

(i) Ascertainment of Total Purchases:

Total purchases are calculated by adding cash and credit purchases. Cash purchases, are given in Cash Book. Credit purchases are calculated by preparing total creditors account. The specimen of Total Creditors Account is given below:

Dr. Total Creditors Account Cr.

| Particulars | Amount

Rs. |

Particulars |

Amount Rs. |

| To Cash paid | ……… | By Balance b/d | ……… |

| To Discount Received | ……… | (Opening Balance) | ……… |

| To Purchases Returns | ……… | By Credit Purchases | ……… |

| To Balance c/d | ……… | (balancing figure) | |

| (Closing Balance) | |||

| ……… | ……… |

Look at the following illustration and see how total purchases have been found out.

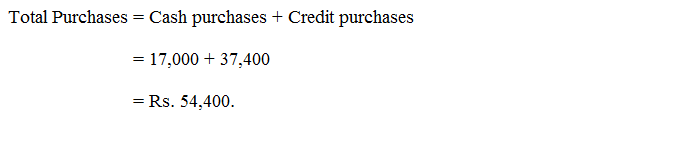

Illustration: From the following information, you are required to calculate total purchases:

| Rs. | |

| Cash purchases | 17,000 |

| Creditors as on April 1, 2002 | 8,000 |

| Cash paid to creditors | 31,000 |

| Purchases return | 1,000 |

| Creditors as on March 31, 2003 | 13,400 |

Solution:

Dr. Total Creditors Account Cr.

| Particulars | Amount

Rs. |

Particulars | Amount

Rs. |

| To Cash paid | 31,000 | By Balance b/d (Opening Balance) | 8,000 |

| To Purchases return | 1,000 | By Credit Purchases (Balancing Figure) | 37,400 |

| To Balance c/d (Closing Balance) | 13,400 | ||

| 45,400 | 45,400 |

(ii) Ascertainment of Total Sales:

Total sales are calculated by adding cash and credit sales. Cash sales are given in cash book. For ascertaining the amount of credit

sales, the total debtors account should be prepared. The specimen of total debtors account is given below:

Dr. Total Debtors Account Cr.

| Particulars | Amount Rs. | Particulars | Amount Rs. |

| To Balance b/d (Op. Bal.) | ……… | By Cash received | ……… |

| To Credit Sales (Bal. Fig.) | ……… | By Discount Allowed | ……… |

| By Sales Returns | ……… | ||

| By Balance c/d (Clo. Bal.) | ……… | ||

| ……… | ……… |

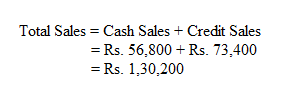

Illustration :

From the following facts you are required to calculate total sales made during the period:

| Particulars | Amount

Rs. |

Particulars | Amount

Rs. |

| Sundry Debtors as on April 1, 2002 | 20,400 | Sundry Debtors as on March 31, 2003 | 27,600 |

| Cash received from Sundry Debtors | 60,800 | Cash Sales | 56,800 |

| Sales Return | 5,400 |

Dr. Total Debtors Account Cr.

| Particulars | Amount

Rs. |

Particulars | Amount

Rs. |

| To Balance b/d (Op. Bal.) | 20,400 | By Cash received | 60,800 |

| To Credit Sales (Bal. Fig.) | 73,400 | By Sales Return | 5,400 |

| By Balance c/d (Clo. Bal.) | 27,600 | ||

| 93,800 | 93,800 |

(iii) Ascertainment of balances of sundry debtors and sundry creditors:

If credit sales and credit purchases are given, the opening or closing balances of debtors and/or creditors can be ascertained by preparing total debtors account and total creditors accounts.

Illustration :

From the following particulars, calculate closing balances Debtors and Creditors:

| Rs. | |

| Sundry Debtors as on 1.4.2001 | 28,680 |

| Sundry Creditors as on 1.4.2001 | 41,810 |

| Credit purchases | 1,51,400 |

| Credit sales | 1,65,900 |

| Discount earned | 5,200 |

| Discount allowed | 4,800 |

| Return outwards | 7,440 |

| Return inwards | 6,444 |

| Cash received from debtors | 1,50,536 |

| Cash paid to creditors | 1,43,765 |

Solution:

Dr. Total Debtors Account Cr.

| Particulars | Amount

Rs. |

Particulars | Amount

Rs. |

| To Balance b/d (1.4.2001) | 28,680 | By Return inwards | 6,444 |

| To Credit Sales | 1,65,900 | By Cash received | 1,50,536 |

| By Discount allowed | 4,800 | ||

| By Balance c/d (Balancing figures) | 32,800 | ||

| 1,94,580 | 1,94,580 |

| To Balance b/d | 32,800 |

Dr. Total Creditors Account Cr.

| Particulars | Amount

Rs. |

Particulars | Amount

Rs. |

| To Return outwards | 7,440 | By Balance b/d (1.4.2001) | 41,810 |

| To Cash paid | 1,43,765 | By Credit Purchases | 1,51,400 |

| To Discount received | 5,200 | ||

| To Balance c/d(Balancing figures) | 36,805 | ||

| 1,93,210 | 1,93,210 | ||

| By Balance b/d | 36,805 |

Illustration :

From the following details, find out Credit Sales for the year.

| Rs. | |

| Opening balance of Sundry Debtors | 30,000 |

| Cash received during the year | 2,05,000 |

| Closing balance of Sundry debtors | 48,000 |

| Discount allowed | 13,000 |

| Goods returned by Customers | 14,000 |

Solution:

Dr. Total Debtors Account Cr.

| Particulars | Amount

Rs. |

Particulars | Amount

Rs. |

| To Balance b/d | 30,000 | By Cash received | 2,05,000 |

| To Credit sales (Balancing figure) | 2,50,000 | By Discount allowed | 13,000 |

| By Sales Return | 14,000 | ||

| By Balance c/d | 48,000 | ||

| 2,80,000 | 2,80,000 |

Illustration :

From the following details find out Credit Purchases.

| Rs. | |

| Opening balance of Sundry Creditors | 50,000 |

| Closing balance of Sundry Creditors | 60,000 |

| Cash paid | 2,65,000 |

| Discount received | 15,000 |

| Purchase returns | 15,000 |

Solution:

Dr. Total Creditors Account Cr.

| Particulars | Amount

Rs. |

Particulars |

Amount Rs. |

| To Cash paid | 2,65,000 | By Balance c/d | 50,000 |

| To Discount received | 15,000 | By Credit Purchases (Balancing figure) | 3,05,000 |

| To Purchase return | 15,000 | ||

| By Balance c/d | 60,000 | ||

| 3,55,000 | 3,55,000 |

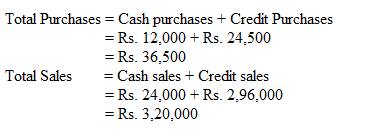

Illustration :

Find out total purchases and total sales from the following details by making necessary accounts:

| Rs. | |

| Opening balance of Sundry debtors | 50,000 |

| Opening balance of Sundry creditors | 30,000 |

| Cash collected from Sundry debtors | 3,00,000 |

| Discount received | 1,500 |

| Cash Paid to Sundry creditors | 20,000 |

| Discount allowed | 5,000 |

| Return inwards | 6,000 |

| Return outwards | 8,000 |

| Closing balance of Sundry debtors | 35,000 |

| Closing balance of Sundry creditors | 25,000 |

| Cash Purchases | 12,000 |

| Cash Sales | 24,000 |

Solution:

i) Calculation of Credit Sales

Dr. Total Debtors Account Cr.

| Particulars | Amount

Rs. |

Particulars | Amount

Rs. |

| To Balance b/d | 50,000 | By Cash received | 3,00,000 |

| To Credit Sales (Balancing figure) | 2,96,000 | By Discount allowed | 5,000 |

| By Returns Inwards | 6,000 | ||

| By Balance c/d | 35,000 | ||

| 3,46,000 | 3,46,000 |

ii) Calculation of Credit Purchases

Dr. Total Creditors Account Cr.

| Particulars | Amount

Rs. |

Particulars |

Amount Rs. |

| To Discount received | 1,500 | By Balance b/d | 30,000 |

| To Cash paid | 20,000 | By Credit Purchases (Balancing figure) | 24,500 |

| To Return outwards | 8,000 | ||

| To Balance c/d | 25,000 | ||

| 54,500 | 54,500 |

Illustration :

Mr.James commenced business on 1.4.2004 with a Capital of Rs.75,000. He immediately bought furniture for Rs.12,000. During

the year, he borrowed Rs.15,000 from his wife as loan. He has withdrawn Rs.21,600 for his family expenses. From the following particulars you are required to prepare Trading and Profit & Loss A/c and Balance Sheet as on 31.3.2005.

| Rs. | |

| Cash received from Sundry debtors | 1,21,000 |

| Cash paid to Sundry creditors | 1,75,000 |

| Cash Sales | 1,00,000 |

| Cash Purchases | 40,000 |

| Carriage inwards | 4,500 |

| Discount allowed to Sundry debtors | 4,000 |

| Salaries | 5,000 |

| Office Expenses | 4,000 |

| Advertisement | 5,000 |

| Closing balance of Sundry debtors | 75,000 |

| Closing balance of Sundry creditors | 50,000 |

| Closing Stock | 35,000 |

| Closing cash balance | 43,900 |

Provide 10% depreciation on furnitures

Solution:

i) Calculation of Credit Sales

Dr. Total Debtors Account Cr.

| Particulars | Amount

Rs. |

Particulars | Amount

Rs. |

| To Balance b/d | — | By Cash received | 1,21,000 |

| To Credit sales | 2,00,000 | By Discount allowed | 4,000 |

| (Balancing figure) | By Balance c/d | 75,000 | |

| 2,00,000 | 2,00,000 |

ii) Calculation of Credit Purchases

Dr. Total Creditors Account Cr.

| Particulars | Amount Rs. | Particulars | Amount Rs. |

| To Cash paid | 1,75,000 | By Balance b/d | — |

| To Balance c/d | 50,000 | By Credit Purchases Credit (Balancing Figure) | 2,25,000 |

| 2,25,000 | 2,25,000 |

Trading and Profit and Loss Account

Dr. of Mr.James for the year ended 31.3.2005 Cr.

|

Particulars Rs. |

Rs. | Particulars Rs. |

Rs. |

| To Opening Stock |

— |

By Sales | |

| To Purchases: | Cash 1,00,000 | ||

| Cash 40,000 | Credit 2,00,000 | ||

| Credit 2,25,000 |

3,00,000 |

||

|

2,65,000 |

|||

| To Carriage inwards |

4,500 |

By Closing Stock |

35,000 |

|

To Gross Profit c/d |

65,500 |

________ |

|

|

3,35,000 |

3,35,000 |

||

| To Discount allowed |

4,000 |

By Gross Profit b/d |

65,500 |

| To Salaries |

5,000 |

||

| To Office expenses |

4,000 |

||

| To Advertisement |

5,000 |

||

| To Depreciation on furniture |

1,200 |

||

| To Net Profit

(transferred to Capital A/c) |

46,300 |

||

|

65,500 |

65,500 |

Balance Sheet of Mr.James as on 31.3.2005

|

Liabilities |

Rs. | Rs. | Assets | Rs. |

Rs. |

| Capital |

75,000 |

Furniture |

12,000 |

||

| Add: Net Profit |

46,300 |

Less: Depreciation |

__1,200 |

10,800 |

|

|

1,21,300 |

|||||

| Less: Drawings |

21,600 |

99,700 |

Sundry Debtors |

75,000 |

|

| Loan from wife |

15,000 |

Closing Stock |

35,000 |

||

| Sundry Creditors |

50,000 |

Cash |

43,900 |

||

|

1,64,700 |

1,64,700 |

Illustration :

Mrs.Malathy maintained her account books on single entry system. On 1.4.2003 her capital was Rs.2,50,000.

Additional information:

Rs.

| Opening stock |

1 ,25,000 |

| Cash received from Sundry debtors |

25,000 |

| Cash sales |

1,00,000 |

| Cash paid to Sundry creditors |

30,000 |

| Opening Sundry debtors |

20,000 |

| Opening Sundry creditors |

91,500 |

| Business expenses |

60,400 |

| Free hold premises (31.3.2004) |

2,00,000 |

| Furniture (31.3.2004) |

3,600 |

| Closing stock |

1,30,000 |

| Closing Sundry debtors |

40,000 |

| Closing Sundry creditors |

1,00,000 |

| Closing cash balance |

27,500 |

Prepare trading and profit & loss account for the year ended 31.03.2004 and balance sheet as on that date.

Solution:

i) Calculation of credit sales:

Dr. Total Debtors Account Cr.

|

Particulars |

Rs. | Particulars |

Rs. |

| To Balance b/d |

20,000 |

By Cash received |

25,000 |

| To Credit Sales |

45,000 |

By Balance c/d |

40,000 |

| (Balancing figure) | |||

|

65,000 |

65,000 |

ii) Calculation of credit purchases:

Dr. Total Creditors Account Cr.

|

Particulars |

Rs. | Particulars |

Rs. |

| To Cash paid |

30,000 |

By Balance b/d |

91,500 |

| To Balance c/d |

1,00,000 |

By Credit Purchases |

38,500 |

| (Balancing figure) | |||

|

1,30,000 |

1,30,000 |

Trading and Profit & Loss Account of Mrs.Malathy

Dr. for the year ended 31.3.2004 Cr.

|

Particulars |

Rs. | Particular |

Rs. |

| To Opening stock |

1,25,000 |

By Sales: | |

| To Purchases – Credit |

38,500 |

Cash 1,00,000 | |

| To Gross Profit c/d |

1,11,500 |

Credit 45,000 |

1,45,000 |

| By Closing stock |

1 30 000 |

||

|

2 75 000 |

2 75 000 |

||

| To Business expenses |

60,400 |

By Gross Profit b/d |

1,11,500 |

| To Net profit |

51,100 |

||

| (Transferred to capital A/c) | |||

|

1,11,500 |

1,11,500 |

Balance Sheet of Mrs.Malathy as on 31.3.2004

|

Liabilities |

Rs. | Rs. | Assets | Rs. |

Rs. |

| Capitl |

2,50,000 |

Free hold premises |

2,00,000 |

||

| Add: Net profit |

51,100 |

Furniture |

3,600 |

||

|

3,01,100 |

Closing stock |

1,30,000 |

|||

| Sundry Creditors |

1,00,000 |

Sundry Debtors |

40,000 |

||

| Cash in hand |

27,500 |

||||

|

4,01,100 |

4,01,100 |

Illustration :

From the following details, prepare Trading and Profit & Loss account for the period ended 31.3.2004 and a Balance sheet on that date.

|

As on 1.4.2003 |

As on 31.3.2004 |

|

| Stock |

50,000 |

25,000 |

| Sundry Debtors |

1,25,000 |

1,75,000 |

| Cash |

12,500 |

20,000 |

| Furniture |

5,000 |

5,000 |

| Sundry Creditors |

75,000 |

87,500 |

|

Other Details: |

Rs. |

| Drawings |

20,000 |

| Discount received |

7,500 |

| Discount allowed |

5,000 |

| Sundry expenses |

17,500 |

| Cash paid to creditors |

2,25,000 |

| Cash received from debtors |

2,67,500 |

| Sales return |

7,500 |

| Purchase return |

2,500 |

| Cash sales |

2,500 |

Solution:

i) Calculation of opening capital:

Statement of affairs as on 1.4.2003

|

Liabilities |

Rs. | Assets |

Rs. |

| Sundry Creditors |

75,000 |

Stock |

50,000 |

| Sundry Debtors |

1,25,000 |

||

| Cash |

12,500 |

||

| Opening capital |

1,17,500 |

Furniture |

5,000 |

| (Balancing figure) | |||

|

1,92,500 |

1,92,500 |

ii) Calculation of Credit Sales:

Total Debtors Account

Dr. Cr.

|

Particulars |

Rs. | Particulars |

Rs. |

| To Balance b/d |

1,25,000 |

By Discount allowed |

5,000 |

| To Credit sales |

3,30,000 |

By Cash received |

2,67,500 |

| (Balancing figure) | By Sales returns |

7,500 |

|

| By Balance c/d |

1,75,000 |

||

|

4,55,000 |

4,55,000 |

iii) Calculation of Credit Purchases:

Dr Total Creditors Account Cr.

|

Particulars |

Rs. | Particulars |

Rs. |

| To Discount received |

7,500 |

By Balance b/d |

75,000 |

| To Cash paid |

2,25,000 |

By Credit purchases |

2,47,500 |

| To Purchases return |

2,500 |

(Balancing figure) | |

| To Balance c/d |

87,500 |

||

|

3,22,500 |

3,22,500 |

Trading and Profit and Loss Account

Dr. for the year ended 31.3.2004 Cr.

|

Particulars |

Rs. | Rs. | Particulars | Rs. |

Rs. |

| To Opening stock |

50,000 |

By Sales: | |||

| To Purchases |

2,47,500 |

Cash 2,500 | |||

| Less: Purchase | Credit 3,30,000 | ||||

| Returns |

2,500 |

3,32,500 |

|||

|

2,45,000 |

Less: Sales | ||||

| To Gross Profit c/d |

55,000 |

Returns |

7,500 |

||

|

3,25,000 |

|||||

| By Closing Stock |

25,000 |

||||

|

3,50,000 |

3,50,000 |

||||

| To Discount | By Gross | ||||

| allowed |

5,000 |

Profit b/d |

55,000 |

||

| To Sundry | By Discount | ||||

| Expenses |

17,500 |

received |

7,500 |

||

| To Net Profit |

40,000 |

||||

| (Transferred to | |||||

| Capital A/c) | |||||

|

62,500 |

62,500 |

Balance Sheet as on 31.3.2004

|

Liabilities |

Rs. | Rs. | Assets | Rs. |

Rs. |

| Capital |

1,17,500 |

Furniture |

5,000 |

||

| Add: Net Profit |

40,000 |

Sundry Debtors |

1,75,000 |

||

|

1,57,500 |

Closing Stock |

25,000 |

|||

| Less: Drawings |

20,000 |

Cash |

20,000 |

||

|

1,37,500 |

|||||

| Sundry Creditors |

87,500 |

||||

|

2,25,000 |

2,25,000 |