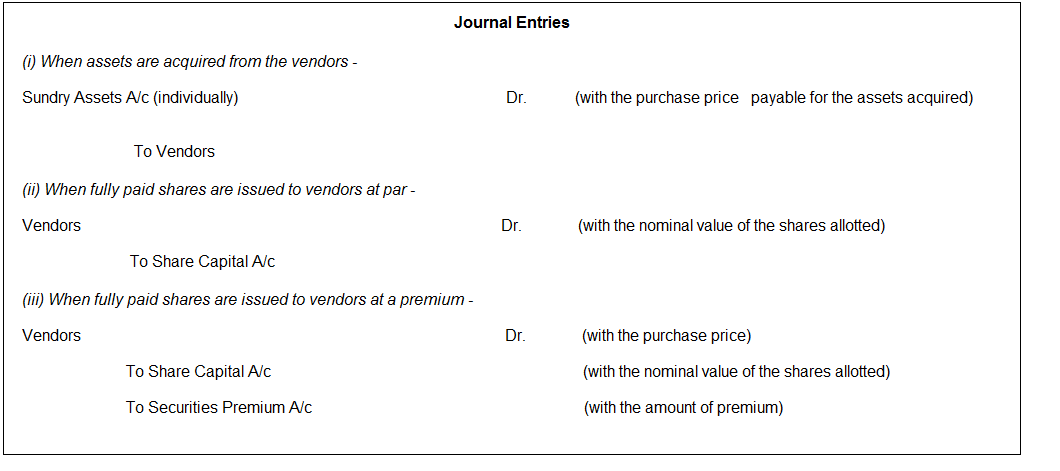

ISSUE OF SHARES TO VENDORS :

A company may purchase assets from the vendors and instead of paying the vendors cash, may settle the purchase price by issuing fully paid shares of the company. This type of issue of shares to the vendors is called issue of shares for consideration other than cash.

Illustration :

Rocket Ltd. purchased the business of Comet Ltd. for Rs.2,70,000 payable in fully paid shares. Rocket Ltd. allotted equity shares of ` 10 each fully paid in satisfaction of the claim by Comet Ltd. Show the necessary journal entries in the books of Rocket Ltd. assuming that:

(a) Such shares are issued at par,

(b) Such shares are issued at premium of 20% and

Solution:

Journal Entries

| Date | Particulars | Dr.(Rs.) | Cr.(Rs.) |

| Sundry Assets Dr. | 2,70,000 | ||

| To Comet Ltd. | 2,70,000 | ||

| (Purchase of assets from Comet Ltd. as per agreement dated…..) | |||

| (a) | If shares are issued at par | ||

| Comet Ltd. Dr. | 2,70,000 | ||

| To Equity Share Capital A/c | 2,70,000 | ||

| (Allotment of 27,000 equity shares of Rs.10 each to vendors as fully paid-up for consideration other than cash as per Board’s resolution dated…) | |||

| (b) | If shares are issued at a premium of 20% | ||

| Comet Ltd. Dr. | 2,70,000 | ||

| To Equity Share Capital A/c | 2,25,000 | ||

| To Securities Premium A/c | 45,000 | ||

| (Allotment of 22,500 equity shares of Rs.10 each at a premium of Rs.2 per share to vendors as fully paid-up for consideration other than cash as per Board’s resolution dated…..) |

Working Notes:

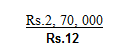

1. When shares are issued at a premium of 20%

Issue price per share = Rs.  = Rs.12

= Rs.12

∴ No. of shares to be allotted =  = Rs.22, 500

= Rs.22, 500