Calculation of New Profit Sharing ratio and Sacrificing Ratio :

When a new partner is admitted, he acquires his share in profits from the old partners. This reduces the old partners’ shares in profit hence, new profit sharing ratio for old partners have to be calculated.

New Profit Sharing Ratio:

The ratio in which all partners (including incoming partner) share the future profits and losses is known as the new profit sharing ratio.

The determination of new profit sharing ratio depends upon the ratio in which the incoming partner acquires his share from the old partners.

New share = Old share – Sacrifice

Sacrificing Ratio:

The ratio in which the old partners have agreed to sacrifice their shares in profit in favour of a new partner is called the sacrificing ratio.

Sacrificing ratio = Old profit sharing ratio – New profit sharing ratio

Sacrifice = Old share – New share

The purpose of this ratio is to determine the amount of compensation (goodwill) to be paid by the new partner to the old partners

for the share of profit surrendered.

From the calculation point of view of sacrificing ratio, the following are the different situations:

1. When the new share of the incoming partner is given.

a) Sacrifice of the old partners are not given (Sacrifice in the old ratio)

b) Unequal sacrifice of the old partners (Unequal sacrifice)

c) Equal sacrifice of the old partners (Equal sacrifice)

d) Entire sacrifice by one of the partners.

2. When the new share of the incoming partner is not given.

– Sacrifice of the old partners are given.

3. New profit sharing ratio is given.

1. When the new share of the incoming partner is given.

a) Sacrifice of the old partners are not given (Sacrifice in the old ratio)

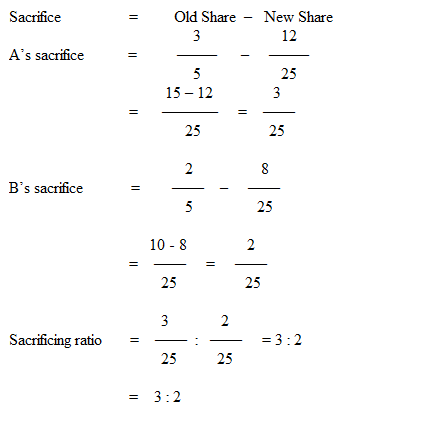

Illustration :

A and B are partners sharing profits in the ratio of 3:2. They admit C for 1/5th share as new partner. Calculate new profit sharing ratio and sacrificing ratio of old partners.

Solution:

a) New Profit Sharing ratio:

b) Sacrificing ratio:

b) Unequal sacrifice of the old partners (Unequal sacrifice)

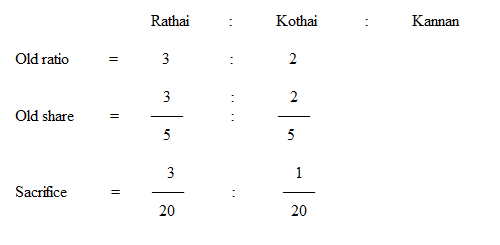

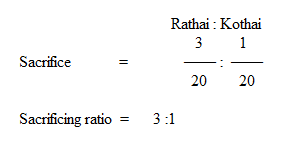

Illustration :

Rathai and Kothai are partners sharing profits in the ratio of 3:2. They admit Kanmani for 1/5th share of future profits which she acquires 3/20th from Rathai and 1/20th from Kothai. Calculate new Profit sharing ratio and sacrificing ratio of old partners.

Solution:

a) New ratio

b. Sacrificing ratio:

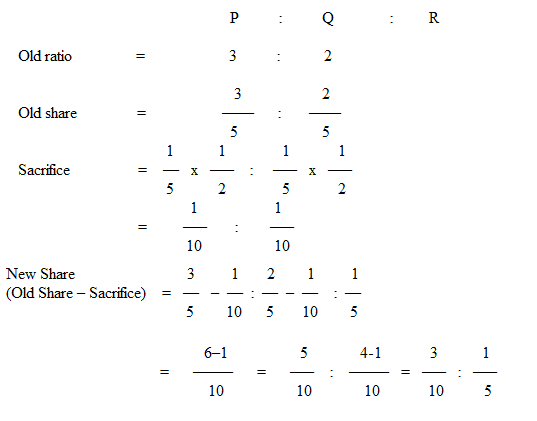

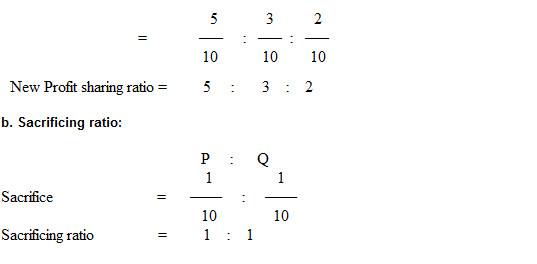

c) Equal sacrifice of the old partners (Equal sacrifice)

Illustration :

P and Q are partners sharing profits in the ratio of 3:2. They admit R for 1/5th Share which acquires equally from P and Q. Calculate new profit sharing ratio and sacrificing ratio of old partners.

Solution:

a) New Profit sharing ratio

d) Entire Sacrifice by one partner only :

Illustration :

G and H are partners sharing profits in the ratio of 3:2. They admit I for 1/5th share which he acquires entirely from G. Calculate a) new ratio and b) Sacrificing ratio.

Solution:

a) New ratio

b. Sacrificing ratio:

Since, only one partner sacrifice his share of profit, it implied that other partner not incurred any loss.

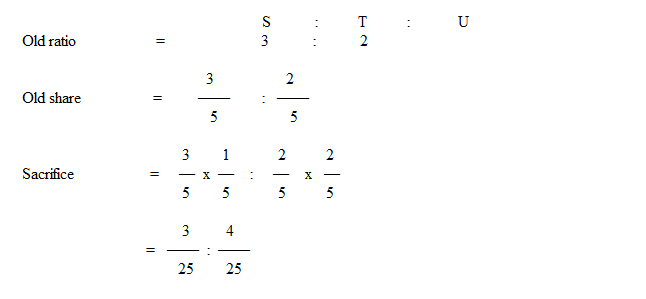

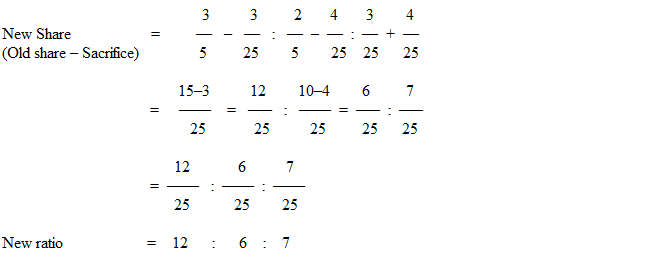

2. When the new share of the incoming partner is not given.

– Sacrifice of the old partners are given.

Illustration :

S and T are partners sharing profits in the ratio of 3:2. They admit U as new partner. which he acquires 1/5th of S’s share and 2/5 of T’sshare. Calculate a) New ratio and b) Sacrificing ratio.

Solution:

a) New ratio :

b. Sacrificing ratio :

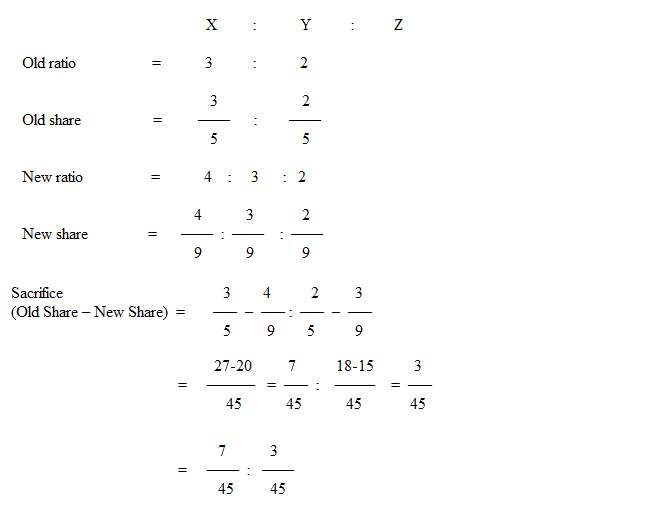

3. New profit sharing ratio is given

Illustration :

X and Y are partners sharing profits in the ratio of 3:2. They admit Z as a new partner. The new profit sharing ratio among X, Y and Z is 4:3:2. Find out the sacrificing ratio.

Solution :

Sacrificing ratio = 7 : 3