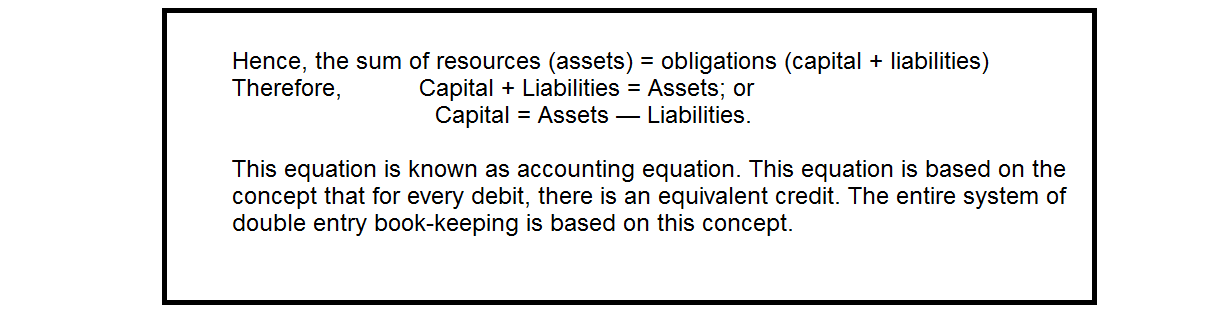

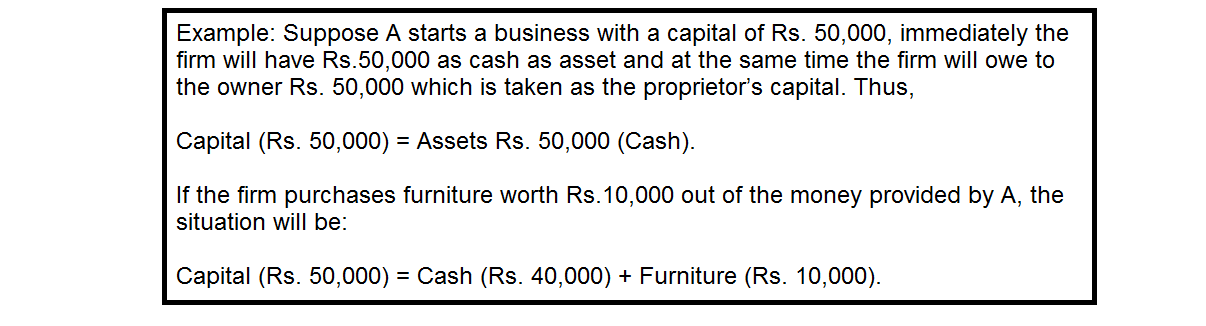

ACCOUNTING EQUATION :

All business transactions are recorded as having a dual aspect. At any point of time, a firm will possess things which may either be sold or converted into cash or which may be later used for a fairly long time. All these things are called assets. Building, land, machinery, furniture, stock, debtors, bills receivable, cash at bank, cash in hand etc. are a few examples of assets. The proprietor of the business brings capital into the business out of which the business (a separate entity) purchases assets for its use. Thus, the amount of the assets of a business is equal to the amount of capital contributed by the proprietor of the business. Thus, Capital = Assets.

In case the capital contributed by the proprietor is insufficient, the business takes borrowing from other parties or outsiders. These parties may give loan or allow credit facilities at the time of purchase of goods. The amounts which are owed to outsiders and which have to be paid, sooner or latter are called liabilities. For example: Loans, Bank Overdraft, Creditors, Bills Payable, and Outstanding Expenses etc. On the one hand, the loan given by the outside parties increases the assets of the business, on the other hand, claims of creditors and lender of money on the assets of the business increase.