ACCOUNTS AND ITS CLASSIFICATION :

The business transactions are recorded in accounts. An account is an individual record of a person, firm, or thing, an item of income or an expense.

An account is prepared for each type of asset, liability, owner(s) equity, revenue and expense. For example, the account of cash would show the cash receipts, cash payments and balance of cash in hand, an account of a person would show the business transactions that have taken place with that person and net position in respect of money owed by or to him.

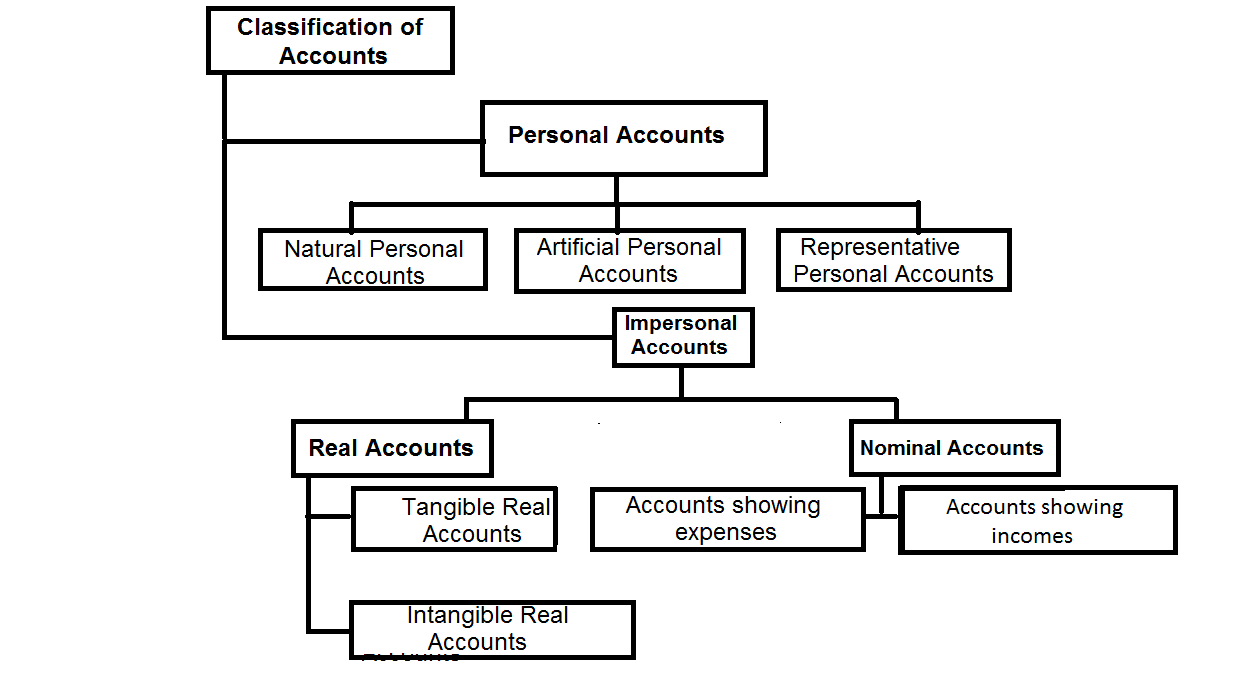

Classification of Accounts

(I) PERSONAL ACCOUNTS: These accounts show the transactions with customers, suppliers, money lenders, the banks and the owner. Personal accounts can take the following forms:

(a) Natural Personal Accounts: The term natural persons means persons who are the creation of God. For example, Naresh a customer or supplier.

(b) Artificial Personal Accounts: These accounts include accounts of corporate bodies or institutions which are recognized as persons in business dealings. For example, any limited company’s account, bank account, insurance company’s account, any firm’s account, any club’s account, etc.

(c) Representative Personal Accounts: These are accounts which represent a certain person or group of persons. In books, the names of the parties will appear. Since these accounts are many in number but are of the same nature, they are added and put under a common title. For example, salary is outstanding towards 15 employees, the amount may be shown against one name ‘Salary Outstanding’ representing all the 15 employees. Interest outstanding, capital account, rent receivable are other such examples.

(II) REAL ACCOUNTS: Real accounts may be of the following types:

(a) Tangible Real Accounts: These are accounts of such things as are tangible i.e. can be seen, touched or felt physically. Examples– land, building, furniture, cash etc. (Note: please note that bank account is a personal account and is not a real account because bank account is the account of some banking company which is an artificial person).

(b) Intangible Real Accounts: These accounts represent such things as cannot be touched but can be measured in terms of money. Example are, goodwill, trade marks, patent rights etc.

(III) NOMINAL ACCOUNTS: Nominal accounts are opened in the books to explain the expenses and incomes. For example, in a business- salary is paid to the employees, rent is paid to the landlord, wages are paid to the workers, commission is paid to the salesmen, wherein cash goes. Example are salary account, rent account, commission account etc. Nominal accounts include accounts of all expenses, losses, income and gains. They are known as nominal as at the end of year these accounts transferredto Trading or P/L Account.