Capital Reserve :

The balance if any in the forfeited share account is a capital profit and will be transferred to ‘Capital reserve account’. The entry for

transferring the balance in the Shares Forfeited Account is

Illustration :

The Directors of a Company after due notice forfeited 100 Shares of Rs.10 each on which the final call money of Rs.3 was not paid. Later these shares were reissued at Rs.8 per share. Pass entries.

Solution:

Journal Entries

| Date | Particulars | L.F | Debit | Credit |

| Share Capital A/c [100 x 10] Dr. | 1,000 | |||

| To Forfeited shares A/c [100 x 7] | 700 | |||

| To Share Final Call A/c [100 x 3] | 300 | |||

| (100 shares forfeited for non payment of final call money) | ||||

| Bank A/c [100 x 8] Dr. | 800 | |||

| Forfeited Shares A/c [100 x 2] Dr. | 200 | |||

| To Share Capital A/c [100 x 10] | 1000 | |||

| (100 Shares reissued at Rs.8) | ||||

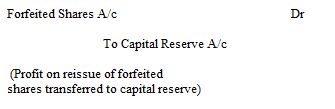

| Forfeited Shares A/c Dr. | 500 | |||

| To Capital Reserve A/c | 500 | |||

| (Profit on reissue of forfeited share transferred to Capital Reserve) |

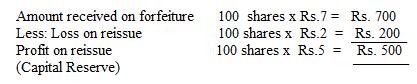

Note : Calculation of profit on reissue.

Illustration :

A company forfeited 200 shares of Rs.10 each on which the first call money of Rs.3 and final call of Rs.2 per share were not received.

These shares were subsequently reissued at Rs.7 per share fully paid up. Pass journal entries for forfeiture and reissue.

Solution:

Journal Entries

| Date | Particulars | L.F | Debit | Credit |

| Share Capital A/c [200 x 10] Dr. | 2,000 | |||

| To Forfeited shares A/c [200 x 5] | 1,000 | |||

| To Share First Call A/c [200 x 3] | 600 | |||

| To Share Final Call A/c. [200 x 2] | 400 | |||

| (200 shares forfeited for non payment of call money) | ||||

| Bank A/c [200 x 7] Dr | 1,400 | |||

| Forfeited Shares A/c [200 x 3] Dr | 600 | |||

| To Share Capital A/c [200 x 10] | 2,000 | |||

| (200 Shares reissued at Rs.7) | ||||

| Forfeited Shares A/c Dr | 400 | |||

| To Capital Reserve A/c | 400 | |||

| (Profit on reissue of forfeited share transferred to Capital Reserve) |