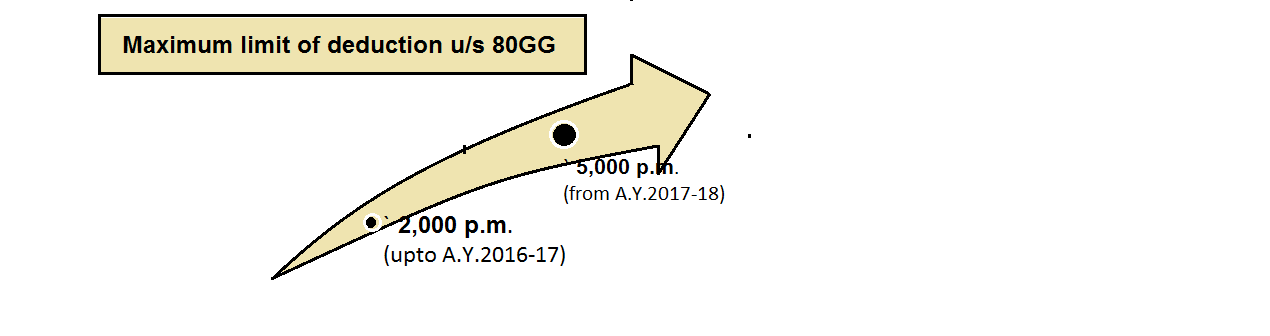

Monetary limit for maximum deduction under section 80GG increased

Effective from: A.Y 2017-18

(i) Under section 80GG, a deduction of any expenditure incurred by an individual (who is not in receipt of house rent allowance from his employer) on payment of rent in respect of any furnished or unfurnished accommodation occupied by him for the purposes of his own residence is allowed, provided he or his spouse or minor child or the HUF of which he is a member does not own a residential house at the place where he ordinarily resides or performs his duties of office or carries on his business or profession.

(ii) The deduction is allowable up to the least of the three limits –

(1) 25% of total income;

(2) Rent paid – 10% of total income;

(3) ` 2,000 per month.

(iii) With a view to provide relief to the individual tax payers who pay rent for the purpose of their own residence, section 80GG has been amended to increase the maximum limit of deduction [third limit given in (ii) above] from ` 2000 per month to Rs.5000 per month.

Example

Mr. Ganesh, a businessman, whose total income (before allowing deduction under section 80GG) for A.Y.2017-18 is ` 4,60,000, paid house rent at ` 12,000 p.m. in respect of residential accommodation occupied by him at Mumbai. Compute the deduction allowable to him under section 80GG for A.Y.2017-18.

Solution

The deduction under section 80GG will be computed as follows:

(i) Actual rent paid less 10% of total income

|

(10 4,60,000) |

||

|

1,44,000 (-) |

……………………………… |

= ` 98,000 (A) |

|

|

100 |

(ii) 25% of total income

|

25 * 4,60,000 |

|

|

……………………………… |

= ` 1,15,000 (B) |

|

100 |

(iii) Amount calculated at ` 5,000 p.m.= ` 60,000 (C)

Deduction allowable (least of A, B and C) = ` 60,000