Procedure of posting :

The procedure of posting is given as follows:

I. Procedure of posting for an Account which has been debited in the journal entry.

Step 1  Locate in the ledger, the account to be debited and enter the date of the transaction in the date column on the debit side.

Locate in the ledger, the account to be debited and enter the date of the transaction in the date column on the debit side.

Step 2 Record the name of the account credited in the Journal in the particulars column on the debit side as “To….. (name of the account credited)”.

Step 3 Record the page number of the Journal in the J.F column on the debit side and in the Journal, write the page number of the ledger on which a particular account appears in the L.F. column.

Step 4 Enter the relevant amount in the amount column on the debit side.

II. Procedure of posting for an Account which has been credited in the journal entry.

Step 1 Locate in the ledger the account to be credited and enter the date of the transaction in the date column on the credit side.

Step 2 Record the name of the account debited in the Journal in the particulars column on the credit side as “By…… (name of the account debited)”

Step 3 Record the page number of the Journal in the J.F column on the credit side and in the Journal, write the page number of the ledger on which a particular account appears in the L.F. column.

Step Enter the relevant amount in the amount column on the credit side.

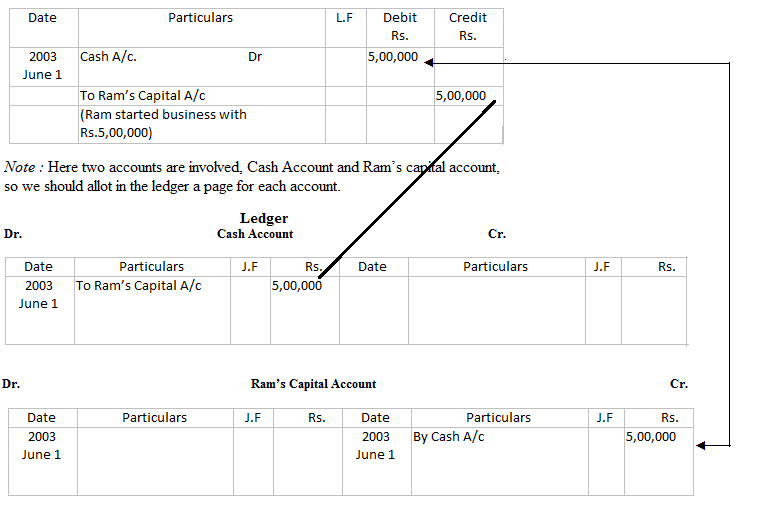

Illustration :

Mr. Ram started business with cash Rs. 5,00,000 on 1st June 2003.

The above transaction will appear in Journal and Ledger as under.

Solution :

In the Books of Ram

Journal

Illustration:

Journalise the following transactions in the books of Amar and post them in the Ledger:-

2004

March1 Bought goods for cash Rs. 25,000

2 Sold goods for cash Rs. 50,000

3 Bought goods for credit from Gopi Rs.19,000

5 Sold goods on credit to Robert Rs.8,000

7 Received from Robert Rs. 6,000

9 Paid to Gopi Rs.5,000

20 Bought furniture for cash Rs. 7,000

Solution : Journal of Amar

|

Date |

Particulars |

L.F |

Debit |

Credit |

||

| 2004 Mar 1 | Purchases A/c Dr.

To Cash A/c (Cash purchases) |

25,000 | — |

25,000 |

— |

|

| 2 | Cash A/c Dr.

To Sales A/c (Cash Sales) |

50,000 | — |

50,000 |

— |

|

| 3 | Purchases A/c Dr.

To Gopi A/c (Credit purchases) |

19,000 |

— |

19,000 |

— |

|

| 5 | Robert A/c Dr.

To Sales A/c (Credit Sales) |

8,000 | — |

8,000 |

— |

|

| 7 | Cash A/c Dr.

To Robert A/c (Cash received) |

6,000 |

— |

6,000 |

— |

|

| 9 | Gopi A/c Dr.

To Cash A/c (Cash paid) |

5,000 |

— |

5,000 |

— |

|

| 20 | Furniture A/c. Dr.

To Cash A/c (furniture purchased) |

7,000 |

— |

7,000 |

— |

|

Explanation : There are six accounts involved: Cash, Purchases, Sales, Furniture, Gopi & Robert, so six accounts are to be opened in the ledger

Ledger of Amar

Cash Account

Dr Cr.

|

Date |

Particulars | J.F | Amount Rs. |

Date | Particulars | J.F |

Amount |

| 2004 |

2004 |

||||||

|

Mar 5 |

To Sales A/c |

50,000 |

Mar 1 |

By Purchases | |||

|

Mar7 |

To Robert A/c |

6,000 |

A/c |

25,000 |

|||

|

Mar 9 |

By Gopi A/c |

5,000 |

|||||

|

Mar 20 |

By Furniture A/c |

7,000 |

Purchases Account

Dr. Cr.

| Date | Particulars | J.F | Amount Rs. |

Date | Particulars | J.F | Amount Rs. |

| ,Mar 1

” 3 |

To Cash A/c To Gopi A/c |

25,000 |

Sales Account

Dr. Cr.

| Date | Particulars | J.F | Amount Rs. |

Date | Particulars | J.F | Amount Rs. |

| 2004 Mar 2

5 |

By Cash A/c By Robert A/c | 50,000

8,000 |

Furniture Account

Dr. Cr.

| Date | Particulars | J.F | Amount Rs. |

Date | Particulars | J.F | Amount Rs. |

| 2004 Mar 20 | To Cash A/c | 7,000 |

Gopi Account

Dr. Cr.

| Date | Particulars | F

J.F |

Amount Rs. |

Date | Particulars | J.F | Amount Rs. |

| 2004 Mar 9 | To Cash A/c | 5,000 | 2004 mar 3 | By Purchase A/c |

19,000 |

Robert Account

Dr. Cr.

| Date | Particulars | F

J.F |

Amount Rs. |

Date | Particulars | J.F | Amount Rs. |

| 2004 Mar 5 | To Sales A/c | 8,000 | 2004 Mar 7 | By Cash A/c | 6,000 |